Study title: Budgets of local government units

The purpose of the study is to provide information on the financial situation of local government unit budgets in terms of income and revenue, expenditure, and costs and other charges.

| Rok |

|---|

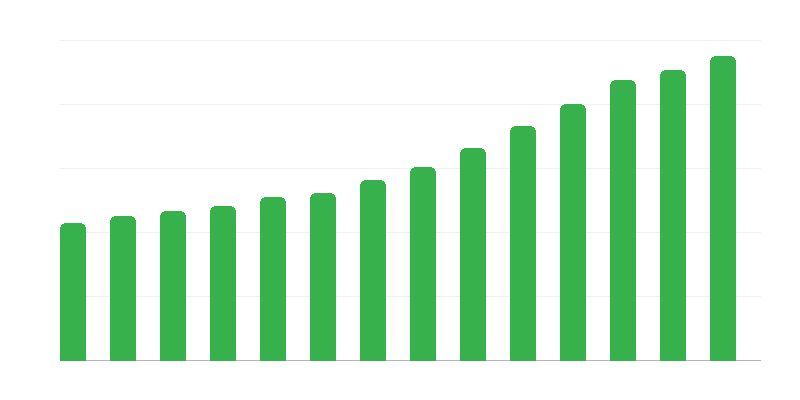

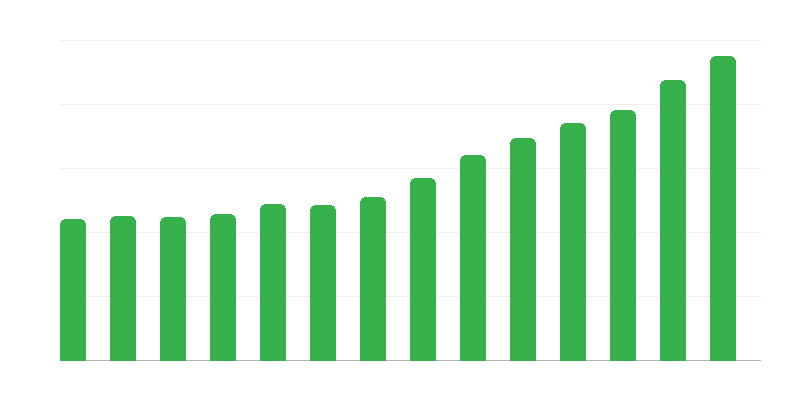

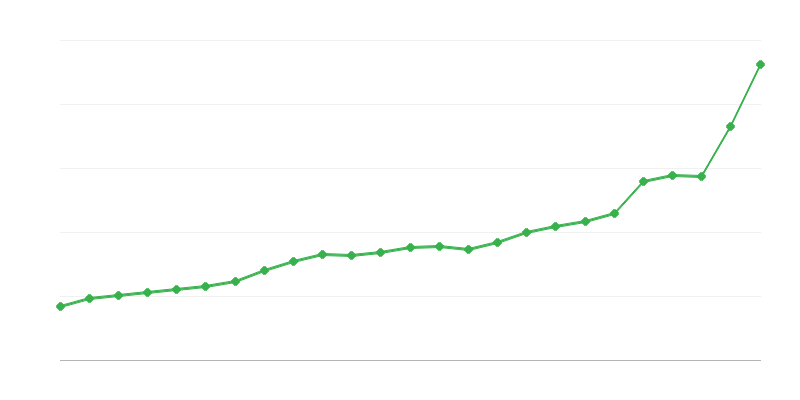

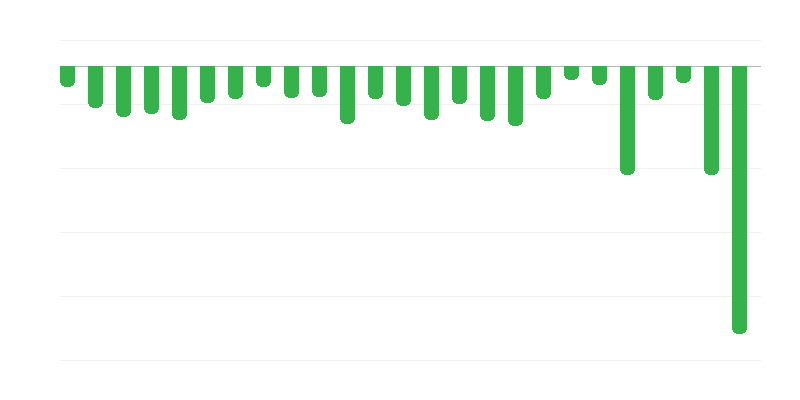

In 2023, public administration expenditures reached 35,073,685.7 thousand PLN, representing an increase of 13.98% compared to the previous year.

Study title: Budgets of local government units

The purpose of the study is to provide information on the financial situation of local government unit budgets in terms of income and revenue, expenditure, and costs and other charges.

An annual plan of revenues and expenditures, as well as incomes and outflows of this unit. Adopted for the budget year. The budget year is the calendar year. The budget resolution serves as the financial management basis for the local government unit during the budget year. The budget resolution consists of: 1) the local government unit budget; 2) attachments. The attachments to the budget resolution include: 1) a summary of planned subsidy amounts granted from the local government unit budget; 2) a revenue account plan of units mentioned in Art. 223 sec. 1, and expenses financed from them; 3) income and cost plans of self-governed budgetary establishments.

They are divided into current expenditures and capital expenditures. Current expenditures of the local government unit budget are understood as budget expenditures that are not capital expenditures. Among current expenditures, in particular, are distinguished: expenditures of budgetary units for salaries and contributions calculated from them, and related to carrying out their statutory activities; subsidies for current tasks; benefits for individuals; payments on account of guarantees and warranties granted by the local government unit, due for repayment in the given budget year; servicing the local government unit's debt; expenditures on programs financed with funds mentioned in Art.5 sec.1 points 2 and 3 of the Public Finance Act, in the part related to the implementation of local government unit tasks. Capital expenditures include expenditures on: investments and investment purchases, including programs financed with funds mentioned in Art.5 sec.1 points 2 and 3, in the part related to the implementation of local government unit tasks; purchase and acquisition of shares and stocks; contributions to commercial law companies.

The data is processed by Content Writer — a limited liability company based in Poland — as part of the independent WorldIndex project. The initiative’s goal is to provide free access to current public data for analyzing trends and better understanding the world.

We also offer commercial access to the WorldIndex API, which provides direct access to data via an API. This allows companies, organizations, and individual users to integrate a real-time information stream into their applications, analytical systems, or AI models.

Data provider: GUS – Department of Macroeconomic and Financial Studies.

The presented information comes from the Domain Knowledge Bases (DBW), maintained by the Polish Central Statistical Office (GUS) and made available under the CC BY 4.0 license.

The chart retrieves data in real time from the DBW API to ensure the most up-to-date and reliable information possible.

If you have detailed questions about the study, we encourage you to contact the data provider directly.

Use reliable data sources with regular updates.

<iframe src="https://contentwriter.hk/worldindex/poland/finance/local-governments/local-government-expenditure-areas/?template=embed-chart" width="100%" height="750" frameborder="0" style="border: none;"></iframe>

The chart was manually prepared and approved by our data analysts.

The chart is connected to the data source, ensuring instant updates.

You can use the above data in your applications via the Polish API data.

Subscribe to WorldIndex for Free